Decoding The 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information

Decoding the 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information

Associated Articles: Decoding the 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information

Introduction

On this auspicious event, we’re delighted to delve into the intriguing subject associated to Decoding the 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information. Let’s weave attention-grabbing info and supply contemporary views to the readers.

Desk of Content material

Decoding the 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information

The 401(ok) plan, a cornerstone of retirement financial savings in the USA, affords vital tax benefits. Nevertheless, these benefits include a stipulation: Required Minimal Distributions (RMDs). Understanding RMDs is essential for retirees, as failing to withdraw the correct quantity can lead to vital tax penalties. This text offers an in depth rationalization of RMDs, together with the way to use a RMD chart, widespread misconceptions, and techniques for managing your withdrawals successfully.

What are Required Minimal Distributions (RMDs)?

RMDs are the minimal quantities you should withdraw yearly out of your 401(ok) and different certified retirement plans (like conventional IRAs and 403(b)s) when you attain a sure age. The aim of RMDs is to make sure that retirement financial savings are finally distributed, stopping tax deferral indefinitely. These withdrawals are topic to revenue tax within the yr they’re acquired.

The Age Issue: When Do RMDs Start?

The age at which you start taking RMDs is essential and has modified over time. At present, the age for starting RMDs is mostly 75, however that is topic to vary, and it is essential to confirm the present guidelines with the IRS. Beforehand, the age was 70 1/2, however this modified in 2020. Those that reached age 70 1/2 earlier than 2020 nonetheless comply with the older guidelines. This highlights the significance of staying up to date on IRS pointers.

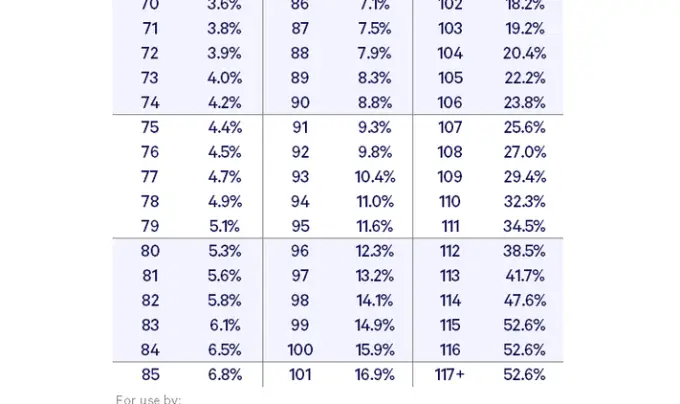

Calculating Your RMD: Utilizing the RMD Chart

The precise quantity of your RMD is set yearly utilizing a formulation primarily based in your account steadiness on the finish of the earlier yr and your life expectancy (or joint life expectancy in case you are married and designate your partner because the beneficiary). The IRS offers tables (also known as RMD charts) that simplify this calculation. These charts are primarily based on actuarial tables that replicate common life expectations.

When you can manually calculate your RMD utilizing the IRS formulation, most monetary establishments will calculate and robotically distribute your RMD for you. Nevertheless, understanding the underlying calculation is crucial for knowledgeable decision-making. The chart itself is basically a lookup desk. You find your age and discover the corresponding distribution share. This share is then utilized to your account steadiness on the finish of the earlier yr to find out your RMD.

Instance utilizing a Hypothetical RMD Chart:

Let’s assume a simplified RMD chart (Word: That is for illustrative functions solely and doesn’t replicate precise IRS tables):

| Age | Distribution Share |

|---|---|

| 75 | 3.6% |

| 76 | 4.0% |

| 77 | 4.4% |

| 78 | 4.8% |

| 79 | 5.2% |

In case your 401(ok) steadiness on the finish of 2023 was $500,000 and also you turned 75 in 2024, your RMD for 2024 can be: $500,000 x 0.036 = $18,000.

Necessary Issues When Utilizing the RMD Chart:

- The chart is restricted to the yr: The IRS updates the life expectancy tables yearly. Subsequently, you should use the chart comparable to the yr by which you’re calculating your RMD. Utilizing an outdated chart will result in incorrect calculations.

- Beneficiary designation: The RMD calculation adjustments in case you are married and select to call your partner as your beneficiary. The distribution percentages will probably be primarily based on joint life expectancy, leading to decrease RMDs within the preliminary years.

- Account steadiness fluctuations: The RMD is predicated in your account steadiness on the finish of the earlier yr. Market fluctuations can considerably influence your RMD from yr to yr.

- A number of accounts: If in case you have a number of retirement accounts (e.g., a 401(ok) and a standard IRA), you should calculate the RMD for every account individually.

Penalties for Failing to Take RMDs:

The IRS imposes a hefty penalty for failing to take your required minimal distribution. The penalty is a whopping 50% of the quantity it is best to have withdrawn however did not. This may considerably cut back your retirement revenue and create a considerable tax burden. This penalty isn’t one thing to be taken evenly.

Methods for Managing RMDs:

- Tax diversification: Take into account spreading your RMD withdrawals throughout completely different tax brackets to attenuate your total tax legal responsibility.

- Tax-loss harvesting: If in case you have capital losses in your taxable accounts, you need to use them to offset a few of the tax legal responsibility out of your RMDs.

- Charitable donations: Certified Charitable Distributions (QCDs) let you instantly donate as much as $100,000 out of your IRA to a certified charity with out having to incorporate the distribution in your taxable revenue. This technique is especially helpful for these in increased tax brackets.

- Monetary planning: Seek the advice of with a monetary advisor to develop a complete retirement plan that addresses your RMDs and different retirement revenue sources. They may also help you create a withdrawal technique that aligns along with your monetary objectives and danger tolerance.

Widespread Misconceptions about RMDs:

- RMDs are solely for many who are retired: Whereas most individuals start taking RMDs after retirement, this isn’t strictly true. The age requirement is the figuring out issue, not your employment standing.

- RMDs are all the time a set share: The share used to calculate your RMD adjustments yearly and is predicated in your age and life expectancy.

- You’ll be able to select to delay RMDs: You can not delay RMDs past the required age with out incurring vital penalties.

- RMDs are solely relevant to 401(ok)s: RMDs apply to numerous certified retirement plans, together with conventional IRAs, 403(b)s, and others.

Staying Knowledgeable and In search of Skilled Recommendation:

The data supplied right here is for instructional functions solely and shouldn’t be thought of monetary recommendation. The tax legal guidelines and laws surrounding RMDs are advanced and topic to vary. It’s essential to remain up to date on the most recent IRS pointers and search skilled recommendation from a certified monetary advisor or tax skilled to make sure you are complying with all relevant laws and creating a sound retirement withdrawal technique tailor-made to your particular person circumstances. They may also help you navigate the complexities of RMDs and create a plan that maximizes your retirement revenue whereas minimizing your tax legal responsibility. Bear in mind, proactive planning is vital to a profitable and financially safe retirement. Do not hesitate to hunt skilled steerage to make sure you make knowledgeable choices relating to your RMDs and your total retirement plan. The penalties for non-compliance are substantial, and the peace of thoughts that comes with correct planning is invaluable. Lastly, all the time confer with the official IRS publications and pointers for essentially the most up-to-date and correct info on RMDs.

-_FI.png)

_Table.png?width=1578u0026name=IRA_Required_Minimum_Distribution_(RMD)_Table.png)

Closure

Thus, we hope this text has supplied precious insights into Decoding the 401(ok) Required Minimal Distribution (RMD) Chart: A Complete Information. We thanks for taking the time to learn this text. See you in our subsequent article!