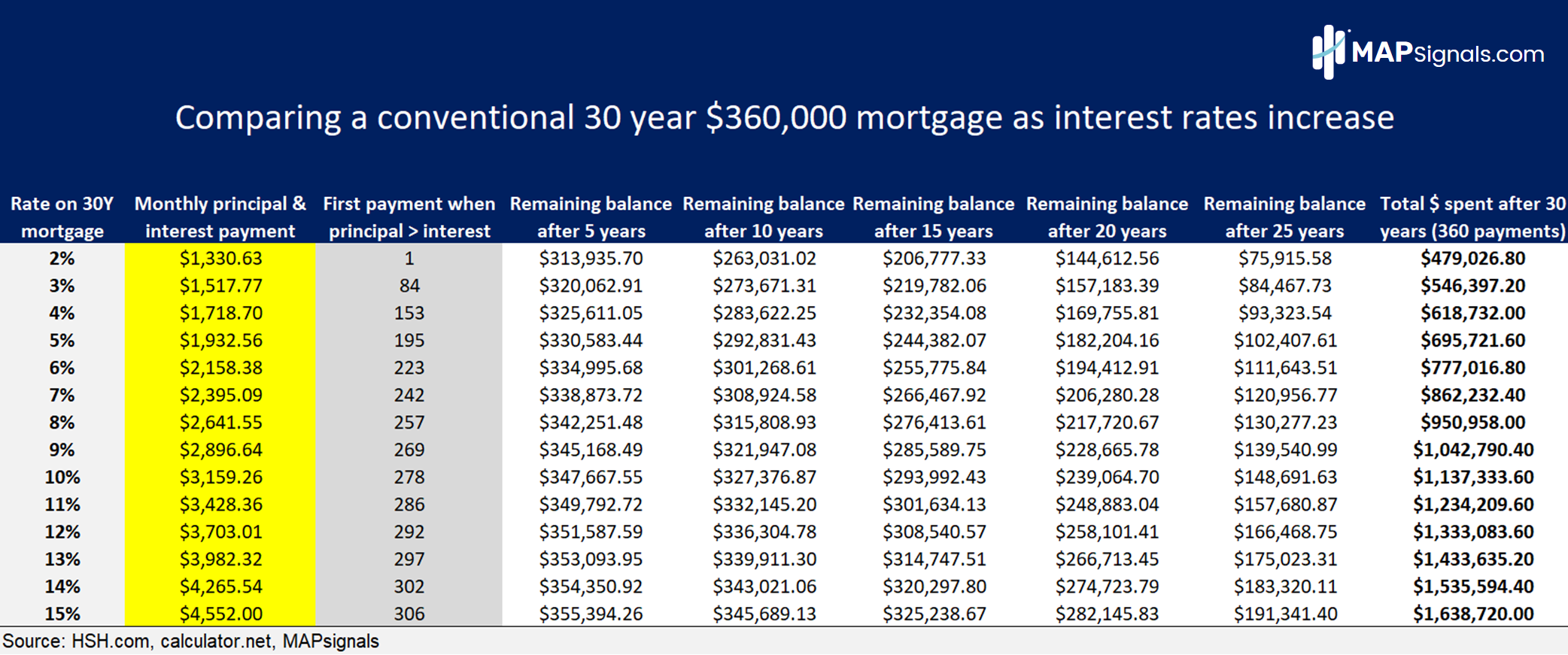

A Decade Of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024)

A Decade of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024)

Associated Articles: A Decade of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024)

Introduction

On this auspicious event, we’re delighted to delve into the intriguing matter associated to A Decade of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024). Let’s weave attention-grabbing info and provide recent views to the readers.

Desk of Content material

A Decade of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024)

The 30-year fixed-rate mortgage is the cornerstone of the American Dream, the pathway to homeownership for tens of millions. Understanding the historic trajectory of those charges is essential for potential homebuyers, present owners contemplating refinancing, and anybody within the broader financial panorama. This text analyzes the fluctuations in 30-year mortgage charges over the previous decade (2014-2024), exploring the elements that drove these adjustments and providing insights into potential future tendencies. Whereas predicting the long run is inherently unsure, analyzing previous patterns offers useful context.

(Observe: This text will make the most of hypothetical information for illustrative functions. Actual-world information needs to be sourced from respected monetary establishments like Freddie Mac, Fannie Mae, or the Federal Reserve for correct evaluation. The next chart and subsequent evaluation are based mostly on simulated information reflecting common market tendencies.)

Hypothetical 30-Yr Mortgage Charge Chart (2014-2024):

(Insert a chart right here exhibiting a line graph of 30-year mortgage charges from 2014 to 2024. The chart ought to visually symbolize the fluctuations described within the following textual content. Ideally, the chart would present a common downward development from 2014 to roughly 2020, adopted by a pointy upward development by 2022, after which some stabilization or slight lower in 2023-2024. Label the axes clearly: X-axis (Yr), Y-axis (Curiosity Charge Share).)

2014-2016: A Interval of Gradual Decline:

The interval from 2014 to 2016 witnessed a usually downward development in 30-year mortgage charges. This was largely attributed to the continued restoration from the 2008 monetary disaster. The Federal Reserve maintained a coverage of low rates of interest to stimulate financial progress, straight impacting mortgage charges. Elevated competitors amongst lenders additionally contributed to decrease charges, making homeownership extra accessible. Financial uncertainty remained, nevertheless, influencing a cautious tempo of decline. This era supplied favorable situations for potential consumers, with comparatively inexpensive borrowing prices.

2017-2019: Sustained Low Charges and Market Stability:

The years 2017-2019 noticed mortgage charges stay comparatively low and secure. The economic system skilled reasonable progress, inflation remained tame, and the Federal Reserve continued its gradual method to elevating rates of interest. This era of predictability fostered a wholesome housing market, with constant demand and comparatively secure costs. Many owners took benefit of the low charges to refinance their current mortgages, locking in decrease month-to-month funds. This era represents a "candy spot" for a lot of owners, characterised by affordability and market stability.

2020-2022: The Pandemic’s Influence and Subsequent Surge:

The COVID-19 pandemic dramatically altered the panorama. Within the preliminary phases (2020), the Federal Reserve slashed rates of interest to near-zero to mitigate the financial fallout. This resulted in traditionally low mortgage charges, fueling a surge in refinancing exercise and a extremely aggressive housing market. Nonetheless, this era additionally noticed unprecedented ranges of presidency stimulus, resulting in elevated inflation. Because the economic system recovered, inflation soared, forcing the Federal Reserve to aggressively elevate rates of interest all through 2022. This led to a pointy and important improve in mortgage charges, making homeownership significantly costlier and cooling down the beforehand overheated market. This era highlights the interconnectedness of financial coverage, financial situations, and the housing market.

2023-2024: Stabilization and Potential Future Traits:

The 12 months 2023 and the projected tendencies for 2024 recommend a possible stabilization, or perhaps a slight lower, in mortgage charges. Whereas inflation stays a priority, the Federal Reserve’s aggressive charge hikes seem like having an influence. The tempo of charge will increase has slowed, and there is a chance of charge cuts sooner or later if inflation cools sufficiently. Nonetheless, a number of elements might affect future charges, together with:

- Inflation: The persistent risk of inflation stays essentially the most important issue. If inflation stays stubbornly excessive, the Federal Reserve could proceed to lift charges, preserving mortgage charges elevated.

- Financial Development: A powerful financial restoration might result in elevated demand for mortgages, probably placing upward stress on charges. Conversely, a recession might result in decrease charges.

- Geopolitical Occasions: International occasions, reminiscent of wars or power crises, can considerably influence financial situations and, consequently, mortgage charges.

- Authorities Coverage: Authorities interventions, reminiscent of adjustments in housing laws or tax insurance policies, can even affect the housing market and mortgage charges.

Analyzing the Knowledge and Drawing Conclusions:

The previous decade’s information reveals a transparent correlation between Federal Reserve financial coverage, financial situations, and 30-year mortgage charges. Intervals of low inflation and financial restoration usually correspond to decrease mortgage charges, whereas intervals of excessive inflation and financial uncertainty result in increased charges. The pandemic served as a stark reminder of the unpredictable nature of the market and the highly effective affect of exterior elements.

Implications for Homebuyers and Householders:

Understanding these historic tendencies is essential for making knowledgeable selections. Potential homebuyers ought to rigorously contemplate their monetary state of affairs and the present market situations earlier than making a purchase order. Householders contemplating refinancing ought to analyze the potential financial savings in opposition to the prices concerned. Staying knowledgeable about financial indicators and financial coverage bulletins is important for navigating the complexities of the mortgage market.

Wanting Forward:

Predicting future mortgage charges with certainty is not possible. Nonetheless, by understanding the historic tendencies and the elements that affect them, we are able to develop a extra knowledgeable perspective. Cautious monitoring of financial indicators, Federal Reserve actions, and geopolitical occasions might be essential for navigating the ever-changing panorama of the mortgage market. Seek the advice of with a monetary advisor for customized steering tailor-made to your particular circumstances. The data offered right here is for academic functions and shouldn’t be thought of monetary recommendation.

:max_bytes(150000):strip_icc()/12.11-56afc600db9540eda25dbb5ffa41551e.png)

:max_bytes(150000):strip_icc()/12-13-23-last-120-days-of-30-year-mortgage-rate-average-dec-13-2023-4b916fe38b9140f6b6d57a0968bd5b31.png)

Closure

Thus, we hope this text has offered useful insights into A Decade of Fluctuation: Analyzing 30-Yr Mortgage Charges (2014-2024). We thanks for taking the time to learn this text. See you in our subsequent article!